CrowdHealth Review:

A Smarter Way to Handle Healthcare Costs?

An honest, in-depth look at how CrowdHealth works, who it's perfect for, and who should stick with traditional insurance.

Is CrowdHealth Right for You?

Answer these 4 questions to find out instantly.

1.Are you generally healthy with no major chronic conditions?

2.Are you comfortable being a 'self-pay' patient and occasionally negotiating?

3.Are you under 65 and a non-smoker?

4.Can you handle a $500 out-of-pocket per health event?

What Is CrowdHealth, Exactly?

CrowdHealth is a healthcare crowdfunding platform that launched in 2021 as a modern alternative to both traditional health insurance and religious health-sharing ministries. Founded by Andy Schoonover (Stanford GSB, former CEO of VRI) in Austin, Texas, the company has raised $12 million in funding and grown to approximately 10,000 active members (with 28,000+ total sign-ups since founding).

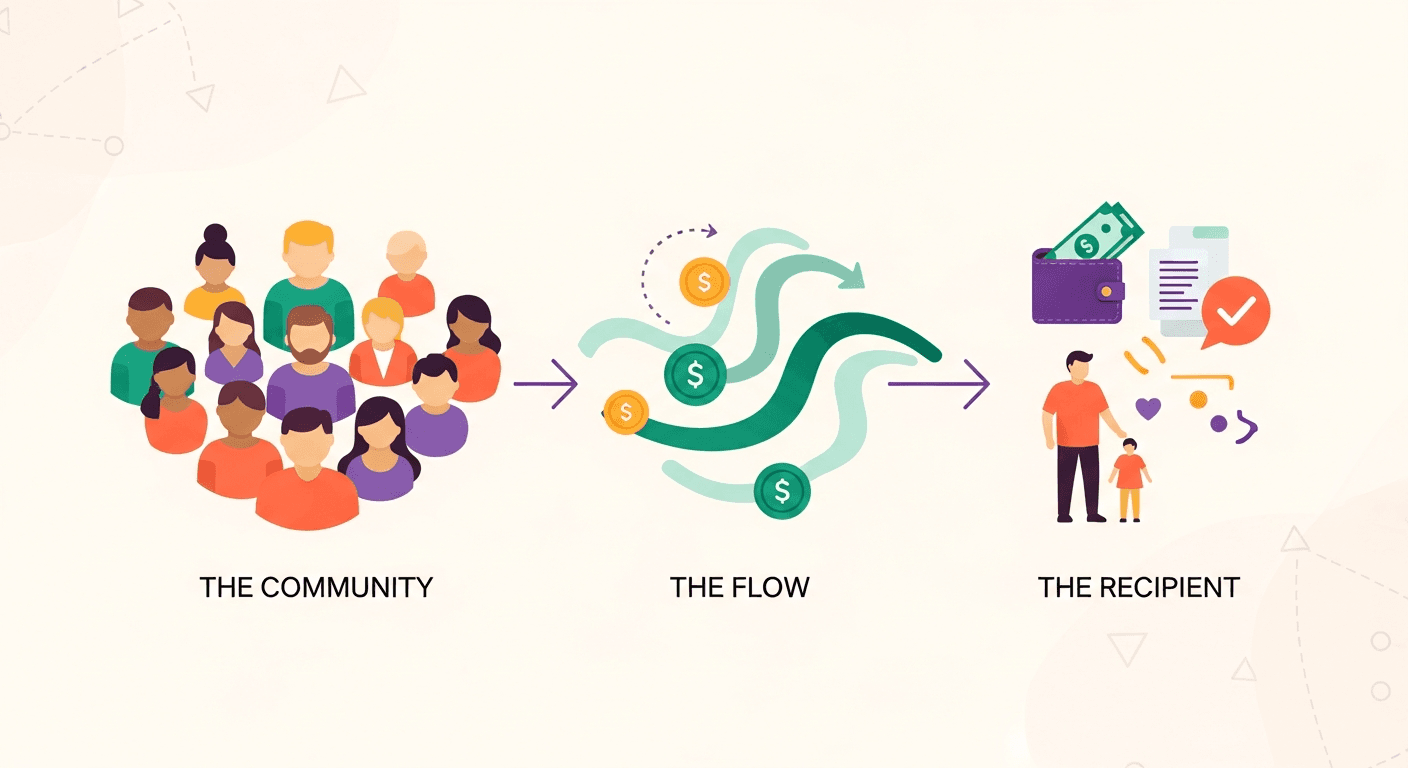

Here's the core idea: instead of paying premiums to an insurance company that profits by denying your claims, you join a community of members who fund each other's medical bills directly. CrowdHealth provides the technology platform, bill negotiation services, and care advocacy to make this work.

CrowdHealth is explicitly NOT insurance. You won't get an insurance card. You'll present as a "self-pay" patient at doctors and hospitals. This is actually an advantage in many cases—cash-pay patients often get significant discounts, and CrowdHealth's team helps negotiate bills down by 30-80% before you ever have to pay.

Key Differentiators

- No religious requirements–Unlike Medi-Share or Samaritan Ministries, CrowdHealth is secular

- Modern tech stack–Mobile app for submitting bills, tracking health events, accessing virtual care

- Transparent funding–Money goes directly into your crowdfunding bank account, not a pooled fund

- Bill negotiation included–Care Advocates negotiate with providers on your behalf

- Virtual care included–Primary care, urgent care, and talk therapy via the app

How CrowdHealth Actually Works

A simple, transparent process that puts you in control of your healthcare.

Join and Set Up

You sign up, verify your identity, and open a crowdfunding bank account (held at Regent Bank, FDIC-insured). Download the app and get oriented with the platform.

Pay Your Monthly Fees

You pay a $60/month Advocacy Fee. You'll also contribute to the crowdfunding pool each month—up to $140-$420 depending on family size.

Something Happens (A "Health Event")

You break your arm, need surgery, or have a medical issue. This is called a "health event" in CrowdHealth terms.

Present as Self-Pay

You go to the doctor or hospital and tell them you're self-pay (no insurance). Request to be billed after care so CrowdHealth can negotiate first.

Submit Your Bills

Upload bills and receipts to the CrowdHealth app. Attach them to your health event. The team reviews everything.

CrowdHealth Negotiates

Your Care Advocate negotiates with providers. CrowdHealth claims they typically reduce bills by 30-80% for planned care and up to 95% for emergency situations.

Pay Your $500 Commitment

You're responsible for the first $500 per health event. For pregnancy, it's $3,000 total for the entire pregnancy journey.

The Community Funds the Rest

Your eligible expenses above $500 get submitted to the community. Other members approve funding requests monthly. The money goes directly into your account to pay bills.

Real Example from CrowdHealth:

A member had a $500,000 emergency bill. After negotiation, it was reduced to ~$150,000. The member paid their $500 commitment. The remaining balance was funded by 1,111 community members contributing $140 each.

What Does CrowdHealth Cost?

| Category | Under 55 | 55+ | Family of 4+ |

|---|---|---|---|

| Advocacy Fee | $60/mo | $60/mo | $60/person/mo |

| Max Crowdfunding Ask | $140/mo | $280/mo | $420/mo |

| Max Monthly Total | $200/mo | $340/mo | $660/mo |

| Avg Actual (2025) | $140/mo | $226/mo | $476/mo |

| Per-Event Commitment | $500 | $500 | $500 |

Black Swan Option (High-Deductible)

- Member Commitment: $15,000 per health event

- Much lower monthly contributions ($25-$75 max asks)

- Best for: People who want catastrophic-only coverage

- Note: Pregnancy is NOT eligible on this option

vs. ACA Insurance

A bronze ACA plan for a family of 4 can easily cost$1,500-2,500/monthwith $8,000+ deductibles per person. CrowdHealth's$476/month averagewith $500 per-event commitments represents massive savings for healthy families.

Special Promo

New members often get the first 3 months for $99/month per person.

What's Eligible for Crowdfunding?

Eligible for Crowdfunding

- Emergency room visits and urgent care

- Hospital stays and surgeries

- Doctor visits and specialist care

- Diagnostic tests and imaging (X-rays, MRIs)

- Ground ambulance (treated as emergency event)

- Prescriptions tied to eligible health events (12-mo limit)

- Maternity care ($3,000 commitment)

- Newborn care (if added within 30 days)

- Virtual primary & urgent care (included)

- Virtual talk therapy (included)

- Annual wellness visit (up to $300/yr)

- Pelvic floor therapy (pregnancy related)

NOT Eligible

- Pre-existing conditions (Years 1-2: none; Year 3+: capped)

- Long-term maintenance prescriptions (>12 months)

- In-person mental health therapy and addiction rehab

- Fertility treatments, IVF, surrogacy

- Abortion

- Dental (except part of annual wellness)

- Vision (except part of annual wellness)

- Weight loss drugs, hair loss medications

- International air ambulance / evacuation

- Cosmetic procedures

The Pre-Existing Condition Reality

This is the biggest limitation vs. traditional insurance. If you have a documented condition BEFORE joining:

- Years 1-2: Expenses for that condition are NOT eligible

- Year 3+: Eligible but capped at $25,000/year per condition

If you have significant chronic conditions, CrowdHealth is probably not your best option. See "Who Should NOT Join" below.

Included Virtual Care Benefits

Virtual Primary Care

Access a doctor via the app for non-emergency issues. You pay upfront, submit the receipt, and it's fully crowdfundable.

Virtual Urgent Care

For issues that need attention but aren't ER-worthy. Same process—pay, submit receipt, get funded.

Virtual Talk Therapy

Mental health support through the app. No upfront payment required—CrowdHealth generates the crowdfunding request automatically. Standout benefit.

Plus: RX Discount Card — Access prescription discounts through the app. Must use generics when available.

Who Is CrowdHealth Perfect For?

The Healthy Self-Employed

Freelancer, consultant, or small business owner. ACA premiums are eating your income. You're generally healthy and rarely go to the doctor.

The Young Family

Spouse and kids. Everyone's healthy. Traditional family insurance costs $2,000+/month. CrowdHealth's average of ~$476/mo is a game-changer.

The Early Retiree (<65)

Retired early, too young for Medicare, too old for cheap marketplace rates. Healthy, active, need coverage for the unexpected.

Health-Conscious Individual

You eat well, exercise, and take care of yourself. You resent paying $500+/month for insurance you rarely use.

"I Hate Health Insurance"

Burned by denied claims and surprise bills. You want transparent pricing and actual humans who help you.

The Gig Economy Worker

Part-time, gig worker, or between jobs. No employer coverage available. Marketplace plans are too expensive for what you get.

Sound like you? CrowdHealth could save you thousands.

Join CrowdHealth Today →Who Should NOT Join CrowdHealth

Do not join CrowdHealth if you:

- 1Have significant chronic conditions

Diabetes requiring ongoing care, autoimmune diseases, cancer history, heart conditions. The 2-year exclusion and $25k/year cap makes it a poor fit.

- 2Take expensive long-term medications

Specialty drugs, biologics, or meds costing hundreds/month indefinitely. The 12-month supply limit won't work for you.

- 3Are 65 or older

Membership ends at 65. You'll transition to Medicare anyway.

- 4Use tobacco

Smokers and tobacco users are not eligible for membership.

- 5Exceed weight limits

Males over 260 lbs and females over 220 lbs are not eligible (CA/NY exemptions apply).

- 6Need fertility treatments

IVF, egg freezing, and fertility treatments are explicitly excluded.

- 7Can't handle self-pay logistics

If you need to just hand over a card and not think, the self-pay model will frustrate you.

- 8Live in a mandate state & can't afford the penalty

CA, NJ, MA, RI, DC residents may owe tax penalties.

Our honest take:

If any of the above apply to you, stick with traditional insurance—even if it's more expensive. The ACA marketplace, a spouse's employer plan, or COBRA are better options for your situation.

CrowdHealth vs. Traditional Health Insurance

| Factor | CrowdHealth | Traditional Insurance |

|---|---|---|

| Monthly Cost | $140-476/mo average | $400-2,500/mo typical |

| Deductible | $500 per event | $2,000-8,000+ per year |

| Pre-existing Conditions | Limited (2-yr wait, caps) | Fully covered (ACA) |

| Provider Network | Any provider (self-pay) | In-network only for best rates |

| Bill Negotiation | Included w/ Care Advocates | You're on your own |

| Claims/Funding | Community funded (99.8%) | Insurer decision |

| Regulation | Minimal oversight | Heavy state/federal reg |

| Guaranteed by Law? | No | Yes |

The Fundamental Trade-off

CrowdHealth costs dramatically less but offers less certainty. Insurance costs more but provides legal guarantees and covers pre-existing conditions. For healthy people, CrowdHealth's value proposition is compelling. For people with ongoing health needs, insurance wins.

CrowdHealth vs. Religious Health Sharing

You may have heard of Medi-Share, Samaritan Ministries, or Christian Healthcare Ministries. CrowdHealth operates similarly but with key differences.

Religious Rules

Lifestyle Rules

Technology

Transparency

Bottom Line: If you want health sharing without the religious component, CrowdHealth is your best option.

CrowdHealth vs. Other Alternatives

How does CrowdHealth stack up against other modern health sharing options?

| Feature | CrowdHealth | Sedera | Knew Health | Zion HealthShare |

|---|---|---|---|---|

| Monthly Cost | $60 + $140-420 | $144–$544 | $142+ | $112–$360 |

| Per-Event (IUA) | $500 | $500–$10,000 | $1,000+ | $1,000–$5,000 |

| Pre-Existing | 2-yr wait, then capped | 12-mo wait (symptom free) | Not verified | 12-mo wait (symptom free) |

| Religious Req? | None (Secular) | None | Not verified | None |

| Trustpilot | 5/5 (526) | 4.7/5 | 5/5 (179) | 4.4/5 |

CrowdHealth Wins On:

- Lowest per-event commitment ($500 vs $1k+ usually)

- Highest customer satisfaction ratings

- Best mobile app & tech experience

- Included virtual care & talk therapy

Where Competitors May Win:

- Zion offers lower monthly starting price ($112)

- Sedera/Zion have higher IUA options (lower monthly)

- Some may have shorter pre-existing lookback periods

State Mandate Penalties

CrowdHealth is NOT insurance and likely does NOT satisfy state individual mandates. If you live in these states, check the math.

| State | Potential Penalty (2025) | Calculation |

|---|---|---|

| California | $950/adult, $475/child | Higher of flat amount OR 2.5% of income |

| New Jersey | $695–$4,908 | Sliding scale based on income |

| Massachusetts | Varies | Tied to affordability schedules |

| Rhode Island | ~$58/mo adult | Based on bronze plan costs |

| DC | $795/adult | Higher of flat or 2.5% income |

| Vermont | No penalty | Reporting required only |

Do the Math

Example: In California, a ~$2,850/year penalty for a family is ~$237/month extra. CrowdHealth + Penalty ($476 + $237 = $713) is often STILL cheaper than a $1,500+ insurance premium. But run your own numbers.

What Real Members Are Saying

The $50K Appendectomy

"I am an MD and we use CrowdHealth for insurance in my business. I had acute appendicitis. 9 hour visit to the ER/OR and home for $50K! CrowdHealth had me covered! I highly recommend them."

The $25K/Year Savings

"Health insurance was costing us $25K a year before we received any benefits; CrowdHealth is not only saving us money but is bringing life and humanity back into the whole healthcare experience."

The $550/Month Savings

"CrowdHealth has been a blessing ever since we joined back in 2023. We have saved a lot of money in not having to pay for insurance via my employer to the tune of over $550 a month."

The Honest Review

"Although care coordination is not always perfect and can be a little clunky at times, I have always been reimbursed for my medical expenses beyond $500 member commitment."

What critics say:

- Provider database for cash-pay doctors could be better

- App has occasional clunky moments (Google Play reviews)

- Lab work/annual wellness reimbursements can require follow-up

- Rare negative experiences often involve "runaround" feelings

By The Numbers

The Catches

What CrowdHealth Doesn't Want to Emphasize

1. It's Not Insurance

This matters legally. Insurance companies must pay valid claims. CrowdHealth has no such obligation. The community has funded 99.8% of bills, but there's no guarantee.

2. Pre-Existing Conditions

If you have anything documented before joining, you're looking at 2 years of no coverage for that condition, then caps. Opposite of ACA.

3. You Might Pay Upfront

Unlike insurance where you copay, you might need to pay bills upfront and wait for community reimbursement. Requires cash flow.

4. State Mandate Penalties

Residents of CA, NJ, MA, RI, VT, DC might owe tax penalties for not having 'insurance'.

5. Company Longevity

CrowdHealth launched in 2021. If they go under, your bank account funds are safe (FDIC), but the platform evaporates.

6. Generosity Score

If you consistently decline to fund other members, your own bills may face scrutiny. Designed to stop freeloaders, but adds complexity.

7. Mental Health Limits

Only virtual talk therapy via app is covered. No in-person psychiatry or addiction treatment.

8. Strict Chargeback Policy

Disputing a crowdfunding charge can get your membership terminated.

Frequently Asked Questions

About CrowdHealth: The Company

Key Facts

- Founded: 2021 in Austin, Texas

- CEO: Andy Schoonover (Stanford GSB, ex-VRI CEO)

- Funding: $12M (Series A) from Next Coast & Activate

- Active Members: ~10,000 (Verified March 2025)

- Total Sign-ups: 28,000+

Mission

Founded after Andy Schoonover's personal frustration with ACA marketplace insurance—high premiums and denied claims for his daughter's care. The mission is to decentralized healthcare payment and restore doctor-patient relationships.

Growth & Retention

Our Final Verdict

Yes, for the right person

CrowdHealth is a legitimate, well-funded company offering a genuinely innovative approach. For healthy individuals frustrated with outrageous premiums, it can save thousands while providing better support than many insurance companies.

The Good

- Dramatically lower costs than insurance

- Freedom to choose any provider

- Bill negotiation saves 30-80%

- Transparent, modern platform

- No religious requirements

- Excellent customer reviews (5/5)

- Virtual care & talk therapy included

The Bad

- Not insurance—no legal guarantee

- Pre-existing conditions limited (2yr wait)

- Long-term prescriptions capped

- Requires self-pay mindset/involvement

- State mandate penalties may apply

- Weight restrictions apply

- Startup risk (founded 2021)

Strongly Recommended For:

- Healthy self-employed individuals

- Healthy families tired of $1,500+ premiums

- Early retirees under 65

- Value transparency over guarantees

Proceed With Caution If:

- You have any chronic conditions

- You take ongoing medications

- You're uncomfortable with uncertainty

Not Recommended For:

- Significant pre-existing conditions

- Need comprehensive mental health care

- Smokers or those over 65

- Weight over limits (unless CA/NY)

Ready to Save on Healthcare?

If CrowdHealth sounds like a fit, you can join through our link below. New members often get the first 3 months for $99/month per person.

Or, if you need comprehensive coverage, check out Healthcare.gov